NAEPC Webinars (See All):

Issue 48 – May, 2026

A Novel Twist on the Charitable Remainder Unitrust Rolling Contributions, Income Control, and the CRT-Owned LLC

By: Scott Luhnau, JD, CTFA and James E. Hargrove, Atty, AEP®, CPA

ABSTRACT

This article examines coordinated planning strategies utilizing Charitable Remainder Unitrusts (“CRUTs”) to manage large or staged asset positions while maximizing charitable deduction utilization and controlling income recognition. It explores rolling contribution techniques, Net-Income with Makeup CRUTs (“NIMCRUTs”), and CRT-owned LLC structures within the framework of fiduciary accounting income rules, Treasury regulations, and state principal and income statutes. These approaches provide sophisticated donors with enhanced tax efficiency, flexibility, and long-term charitable impact while remaining compliant with Internal Revenue Code §664.

INTRODUCTION

Charitable Remainder Trusts (“CRTs”) are fundamentally charitable vehicles designed to create significant long-term philanthropic benefit while providing income streams and tax planning efficiencies for donors. For decades, CRUTs have been used to diversify concentrated investment positions, defer capital gains tax, and generate charitable income tax deductions. Traditionally, CRUTs have been funded in a single transaction with highly appreciated assets which are sold by the trust and reinvested to support ongoing unitrust distributions. The donor gets an immediate income tax deduction when the CRUT is funded, and the CRUT makes payments to the donor for a period of years or their lifetime. At the conclusion of the term or the donor’s life, the remainder goes to charity.

While effective in many circumstances, the one-time funding approach often produces significant inefficiencies for high-net-worth clients experiencing large liquidity events or volatile income years. Charitable deductions may far exceed the donor’s ability to utilize them within the five-year carryforward window, resulting in wasted tax benefits. Modern planning increasingly requires more flexible structures that align charitable giving with income timing, actuarial optimization, and long-term financial strategy.

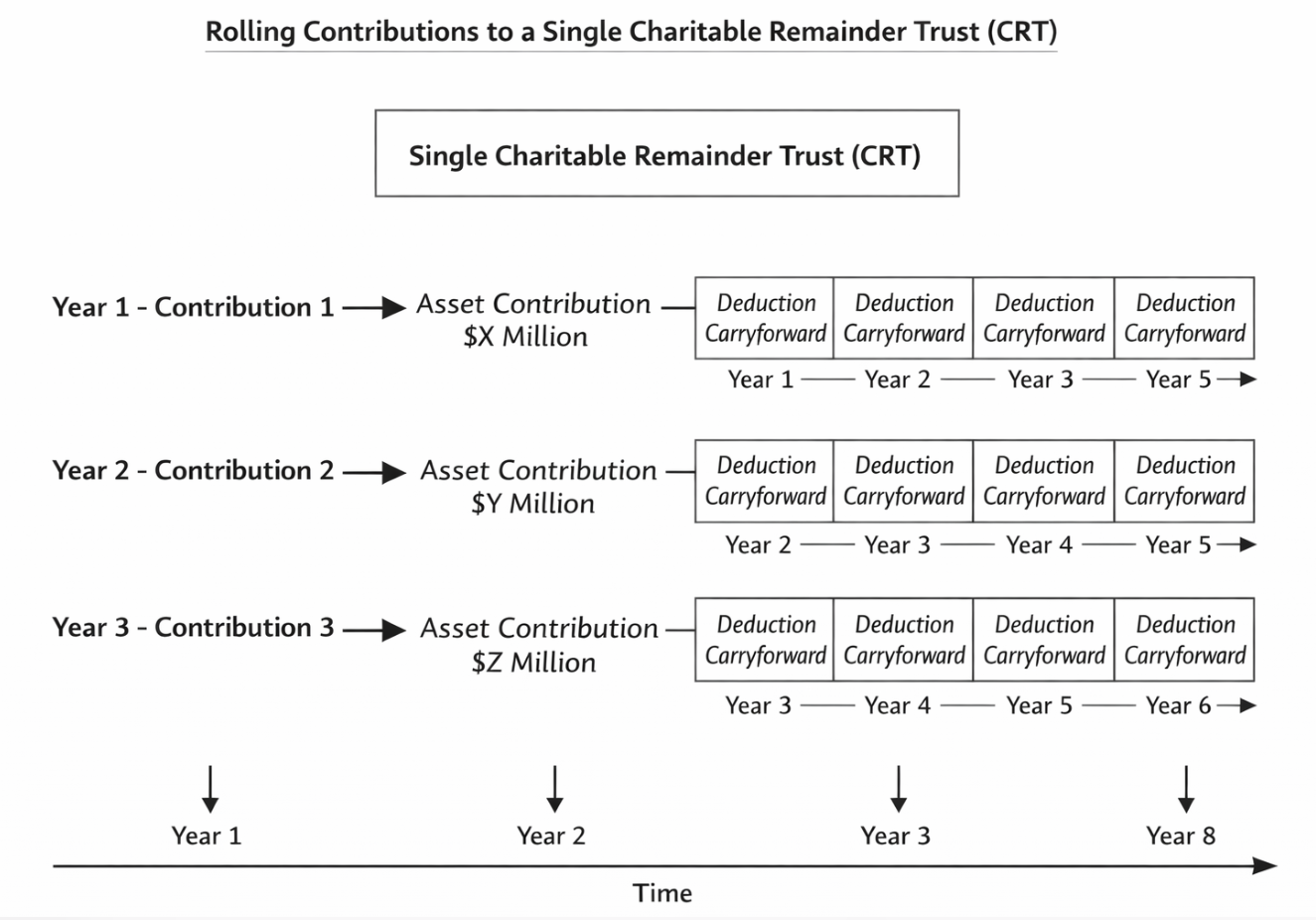

ROLLING CONTRIBUTIONS AND DEDUCTION OPTIMIZATION

Neither Internal Revenue Code §664 nor the Treasury Regulations impose any limitation on the timing or number of contributions to an existing CRUT. Each contribution is treated as a separate gift for valuation and deduction purposes, generating its own charitable income tax deduction based on the actuarial assumptions applicable in the year of funding.

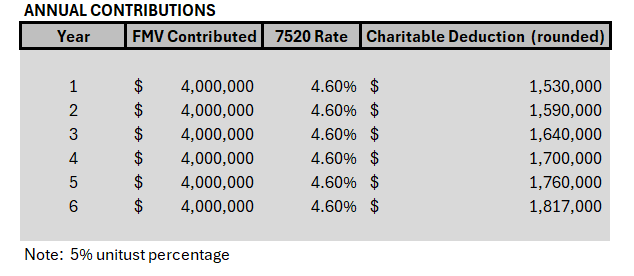

By spreading contributions over successive years, often aligned with the five-year charitable deduction carryforward period, donors can dramatically improve deduction absorption. Rather than generating a single oversized deduction that expires unused, rolling contributions allow deductions to stack efficiently across multiple years. Here is what the strategy could look like (over a 3 year period):

In addition to improved utilization, rolling contributions benefit from actuarial mechanics. The value of the charitable remainder interest increases as the income beneficiary ages. Consequently, successive contributions made in later years generally produce proportionally larger deductions even if contribution amounts remain constant. The actuarial drivers of this increase are primarily the payout rate and donor age, with the Section 7520 rate playing a secondary role.

Example: Assume a donor age 62 holds a concentrated publicly traded stock position valued at $24 million. Rather than contributing the entire position in a single year, the donor contributes $4 million annually to an existing CRUT over six years. Each contribution produces a charitable deduction based on the donor’s age and payout rate at the time of funding. If the donor’s projected adjusted gross income averages $3 million annually, the rolling strategy allows nearly full deduction utilization while improving actuarial efficiency over time.

NIMCRUTS AND FIDUCIARY ACCOUNTING INCOME

A Net-Income with Makeup CRUT (“NIMCRUT”) distributes the lesser of the stated unitrust percentage or fiduciary accounting income (“FAI”). Treasury Regulation §1.643(b)-1 provides that FAI is determined by the governing instrument and applicable state law. This distinction is central to income control strategies.

Unlike a standard CRUT which must distribute the fixed unitrust percentage annually regardless of income generation, a NIMCRUT permits distributions to be deferred in years when FAI is insufficient. Any unpaid unitrust amount accumulates as makeup income and may be distributed in later years when FAI becomes available.

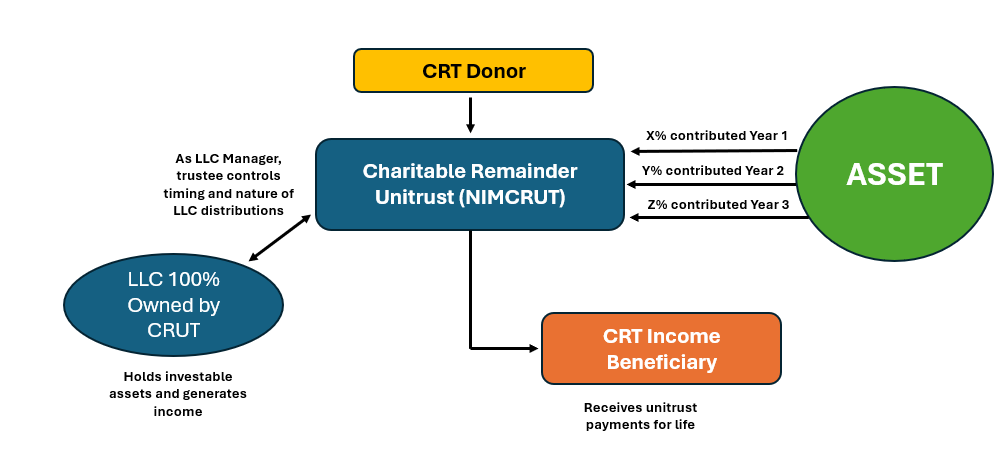

CRT-OWNED LLC STRUCTURE

Where a CRUT holds interests in a pass-through entity such as an LLC taxed as a partnership or disregarded entity, the treatment of income for FAI purposes depends on state fiduciary accounting statutes. In jurisdictions without look-through treatment, income is recognized only upon actual distribution from the entity, allowing trustees to control FAI timing through discretionary distributions.

However, certain states, most notably California, and others adopting modified Uniform Principal and Income Act provisions, may treat undistributed pass-through income as current trust income regardless of distribution. Accordingly, situs selection, governing law provisions, and entity structuring are critical. The strategy requires more than merely defining LLC distributions as income in the trust instrument. Once all these factors are considered, the goal would be to use the LLC as a “spigot” to more proactively manage and reduce the CRUT beneficiary’s income tax exposure.

DISTRIBUTION CHARACTER AND FOUR-TIER SYSTEM

All CRT distributions are governed by the four-tier system under Internal Revenue Code §664(b), which carries out ordinary income, capital gains, tax-free income, and corpus in sequence. A NIMCRUT cannot bypass income tiers or distribute in the absence of FAI. Instead, shortfalls accumulate for future makeup.

INVESTMENT COORDINATION

Although CRTs are exempt from current income taxation, the character and timing of income remain relevant due to the tier system and FAI mechanics. Trustees often pursue long-term growth strategies while selectively realizing gains or triggering LLC distributions to manage income timing and tax character.

CHARITABLE REMAINDER CONSIDERATIONS

Where the charitable remainder is directed to a private foundation rather than a public charity or donor-advised fund, charitable deductions are subject to more restrictive limitations under Internal Revenue Code §170(b). This factor should be incorporated into planning projections.

IRS SCRUTINY AND PROFESSIONAL CAUTION

The IRS has historically examined deferral-oriented NIMCRUT structures, including commentary in Continuing Professional Education materials and public studies announced in the early 2000s. Although no adverse published authority has resulted, conservative implementation remains advisable.

PRACTICAL STRUCTURING NOTE

Many advisors structure the CRT-owned LLC to complete asset sales rather than having the CRT sell directly, minimizing unintended FAI recognition and improving cash flow control.

CONCLUSION

When strategically coordinated, rolling CRUT contributions and NIMCRUT income-control techniques significantly outperform traditional one-time funding approaches. These methods improve deduction utilization, enhance flexibility, and increase long-term charitable impact while remaining compliant with statutory and fiduciary accounting principles.

FOOTNOTES

- I.R.C. § 664(a)-(b).

- Treas. Reg. § 1.643(b)-1.

- Treas. Reg. § 1.664-1(d).

- Uniform Principal and Income Act (various state adoptions).

- I.R.C. § 170(b).