NAEPC Webinars (See All):

Issue 43 – December, 2023

Improving the Tax-Inefficiencies of GRATs with PPLI

By Rajiv Rebello, FSA, CERA

Grantor Annuity Trusts (GRATs) allow clients the ability to move a large amount of assets outside of the estate so that part of the future appreciation of the assets is outside of the estate. However, they also introduce tax-drag and income tax-liabilities that these assets might not otherwise be exposed to. Therefore, the best way to maximize the value of a GRAT is to utilize the GRAT for assets that are tax-inefficient. This holistic estate and investment approach can be improved further by utilizing the GRAT as a vehicle to invest in private placement life insurance (PPLI) which allows the assets to compound without the tax drag. Doing so essentially turns the tax-inefficient assets into tax-efficient assets by providing the client with the benefits of tax-free growth as well as step-up in basis that would be lost if the client only used the GRAT by itself.

THE DOWNSIDES OF GRANTOR ANNUITY TRUSTS

Tax-efficient assets are typically a better fit for investing outside the GRAT (i.e. within the estate) so that these assets can benefit from tax-free growth and step-up in basis. Investing in tax-efficient assets within a GRAT introduces these assets to both tax-drag on the investment growth as well as an income tax-liability on all of the unrealized gains when assets are transferred to the beneficiary. This can negate any estate tax benefits the GRAT provides and end up being worse for the client—as we detailed in depth in a previous article on the topic. I’d strongly recommend those who work with GRATs to read that article so that they can understand why it’s so important to consider the investment, income tax, and wealth management consequences of utilizing a GRAT instead of only focusing on the estate planning elements.

Tax-inefficient assets, on the other hand, are the best fit for utilizing in the GRAT. As discussed in the previous article, investing in these assets through a GRAT allows for the benefit of tax-deferred compounding which can make a significant difference on the after-tax wealth of the client.

However, even if tax-inefficient assets are invested within a GRAT, one key downside of GRAT still remains:

- In order to make GRAT annuity payments back to the grantor, the GRAT must either have realized gains or sell assets in order to make the payment.

Assets within the GRAT often need to be sold in order to make required annuity payments back to the grantor. This tax-drag reduces long-term returns as opposed to just compounding returns for the long-term on a tax-deferred basis (or tax-free with step up in-basis). While the GRAT could make in-kind payments back to the grantor in order to meet the required annuity payments, this would subject the capital appreciation of the assets to the estate tax—which defeats the purpose of establishing the GRAT in the first place. This is another reason why it’s important to utilize tax-inefficient assets within the GRAT as those assets would have annual realized gains that can’t be deferred whether they are inside or outside of the GRAT. - Due to the loss of step-up in basis, all assets within a GRAT are exposed to income taxes on unrealized gains when assets are transferred to the b

While a GRAT helps assets avoid the estate tax, the assets in the GRAT lose the benefit of step-up in-basis that would otherwise be available at death of the grantor. This can expose the assets in the GRAT to state and federal income tax that they otherwise might not be exposed to. This means that the benefits of avoiding the estate tax are minimized since the beneficiaries would still have to pay full federal income and state tax on any unrealized gains that they might otherwise be protected from. Utilizing a GRAT essentially means replacing an estate tax liability with an income tax liability. This is particularly a problem for clients that live in states with high income taxes (eg CA, NY, NJ, etc). Therefore, it’s important to consider the income tax consequences of both the grantor and beneficiary when analyzing whether the GRAT would be beneficial to the client.

Table 1: Benefits and Disadvantages of Investing via a Taxable Account vs a GRAT

While a GRAT allows part of the future appreciation of the assets from estate tax, it exposes these assets to income tax that could otherwise be passed on tax-free via step-up in basis while exposing these assets to additional tax-drag. Therefore, it’s important to evaluate what type of assets are a best fit for the GRAT.

| Estate Planning Tool | Assets Outside of the Estate? | Returns Protected from Estate Tax? | Long-Term Returns Protected From Income Tax Through Step-Up in Basis? | Minimizes Tax-Drag? | Ability to Take Loans for Liquidity? |

| Taxable Account (No GRAT) | x | x | x | ||

| GRAT | x | x | x |

BASE GRAT EXAMPLE

To understand why it’s important to use tax-inefficient assets within a GRAT, it’s helpful to look at an example.

Example 1:

Steve and Kathy are both 60 and live in California and plan on staying there for the rest of their life. They are currently considering moving $50M outside of their estate (those assets have a $30M cost basis). Steve and Kathy already have a high income and therefore don’t need any income from the $50M. Their goal is to pass this $50M so that their kids can sell the assets when they die in the most efficient way possible. They are considering either keeping this money in their estate or using a Zeroed-Out GRAT to minimize the estate taxes owed. Steve and Kathy’s marginal tax rate for short-term capital gains is 54.1% (37% federal tax-rate, plus 3.8% net investment income tax, plus 13.3% state tax rate). The estate tax in 2023 is currently 40% above $25.84 million. Their $50M is primarily invested in private funds with high tax-liabilities and they would like to keep that allocation whether it is in the GRAT or outside the GRAT.

Steve and Kathy are wondering whether it is better to keep the assets in their estate and pay estate tax-rate (40%) or whether to move the money out of their estate and have their beneficiaries pay the full 54.1% short-term capital gains tax-rate on the gains when they die.

Here are the assumptions used in the analysis:

- Steve and Kathy live 30 years and then die. Upon their death, all assets are sold with their beneficiaries receiving the after-tax proceeds.

- Primary asset allocation are low-cost, tax-efficient, equity index funds.

- Asset appreciation rate of 8%.

- $50 million fair market value of assets with $30 million in cost-basis.

- In GRAT analysis this $50M is transferred to the GRAT using the full $25.8M gift exemption and a zeroed out GRAT amount for the remaining $24.2M. A 30 year GRAT is used with a level annuity for simplicity, although in reality shorter-term rolling GRATs would be used (often with a graduated annuity).

- 120% AFR rate (hurdle) of 4.4%.

- Estate Tax Rate of 40%

- Total Short-Term Capital Gains/Ordinary Income Tax Rate of 54.1%.

Table 2: Investing Tax-Inefficient Assets Outside of a GRAT vs Within a GRAT

With tax-inefficient assets, a GRAT helps reduce estate taxes on in-estate assets without introducing extra tax-drag and income tax-liabilities.

| Inside of Estate Assets at Death | Outside of Estate Assets at Death | Total After-Tax Wealth at Death | ||||||

| Market Value of Assets Before Estate Tax ($M) (A) |

Estate Tax Owed ($M) (B) |

Inside of Estate After-Tax Wealth at Death ($M) (C=A+B) |

Outside of Estate Assets Before Income Tax ($M) (D) |

Income Tax Owed ($M) (E) |

Outside of Estate After-Tax Wealth at Death ($M) (F=D+E) |

Total After-Tax Wealth at Death (G=C+F) |

Total After-Tax IRR (H) |

|

| No GRAT | $148 | ($49) | $99 | $0 | $0 | $0 | $99 | 2.30% |

| With GRAT | ($135) | $0 | ($135) | $337 | ($11) | $326 | $191 | 4.57% |

The above table shows the impact of using a GRAT on inside of the estate wealth (Columns A through C), outside of the estate wealth (Columns D through F), and cumulative after-tax wealth(Columns G and H) which summarizes the total after-tax impact of using the GRAT vs not using the GRAT. As Column H shows, if Steve and Kathy wish to invest in tax-inefficient assets, a GRAT offers significantly higher after-tax returns.

This is due to the fact that the GRAT allows for tax-deferred compounding on assets within the GRAT which would not be possible from investing in these assets outside of the GRAT. This reduces the tax-drag of these assets which is significant because with tax-inefficient assets the amount of tax-drag is high.

The net effect here is that John and Mary would have $92M more at death by using the GRAT ($191M vs $99M in Column G) from using a GRAT to invest in these tax-inefficient assets. As such, the after-tax IRR (Column H) of these almost doubles (from 2.30% to 4.57%) by using the GRAT.

Not using the GRAT exposes these assets to heavy tax-drag. If the clients choose not to use the GRAT, then these assets are getting taxed every year at a high 54.1% as well as exposing the estate to estate taxes. So the assets are getting hit by both income and estate taxes. This is why not using the GRAT results in a gross 8% IRR being reduced to a 2.30% IRR after income and estate taxes are taken into consideration.

However, by using the GRAT the assets in the GRAT are allowed to grow tax-deferred while the grantor makes tax payments from outside of the estate which reduces the estate tax significantly. This structure minimizes the tax-drag on the assets. So while the GRAT reduces the after-tax value of the assets inside the estate (from $99M to -$135M as shown in Column C), it significantly improves the after-tax value of the assets in the GRAT (from $0 to $326M as shown in Column F) which more than makes up for the loss on the inside of the estate assets. However, it’s important to note here that the grantor must have assets inside the estate in order to pay the $135M income tax liability.

In the next section we’ll explore why the tax-drag of tax-inefficient assets is so detrimental to long-term after tax returns.

UNDERSTANDING WHY TAX-DRAG IS SO DETRIMENTAL TO RETURNS

To understand why tax-drag is so important to consider, it’s helpful to look at another example.

Example 2:

John and Mary have the choice of investing $1M in two different assets for 30 years. Both assets earn 8% and are taxed at 50%. However Asset A allows for the tax to be paid at the end of the 30 years, while Asset B requires that the 50% tax is paid every year on the gains. Which asset should John and Mary invest in?

Table 3: Performance of Tax-Efficient vs Tax-Inefficient Assets with an 8% expected pre-tax return

By investing in tax-efficient Asset A instead of tax-inefficient Asset B, John and Mary can improve the after-tax return by 47% (from 4.0% to 5.9%).

| After tax value at the end of 30 years | After-Tax IRR | |

| Asset A (Tax at the end of 30 years/Tax-Efficient) | $5,531,328 | 5.9% |

| Asset B (Yearly Tax/ Tax-Inefficient) | $3,243,398 | 4.0% |

As the above table shows, getting taxed 50% at the end of 30 years instead of at the end of each year can lead to 70% more after-tax wealth ($5.5M vs $3.2M). The effect of the annual tax-drag and the reduction in compounding can create a significant impact on the returns of the client. This is why putting tax-inefficient assets within a GRAT is so valuable. Doing so allows investors the ability to minimize the tax-inefficiency of the asset by deferring taxation until the end of the investing period. This is what leads to the returns of investing in tax-inefficient assets via the GRAT being significantly higher than investing in those same assets outside of the GRAT.

THE ESTATE PLANNING BENEFITS OF PPLI

A GRAT helps improve the tax-inefficiency of tax-inefficient assets by allowing for tax-deferred compounding that is protected from the estate tax. However, tax-deferred compounding still creates a tax-liability at the end when the assets are sold and income taxes are finally paid.

That poses the question:

Is there some way to further improve the tax-efficiency of these assets so the tax-deferred benefits can be converted into tax-free benefits?

The answer to that question is yes, by utilizing a private placement life insurance (PPLI) policy with in-kind contributions in combination with a GRAT.

Life insurance policies come with a lot of benefits that are not available with GRATs. Both allow for the assets to grow outside of the estate, but life insurance allows for both tax-free growth and step-up in basis whereas GRATs only allow for tax-deferred growth with no step-up in basis.

Table 4: Comparing Taxable Accounts to GRATs and Life Insurance

Using life insurance as an estate planning tool helps solve for a lot of the tax-inefficiencies embedded in GRATs

| Estate Planning Tool | Assets Outside of the Estate? | Returns Protected from Estate Tax? | Long-Term Returns Protected From Income Tax Through Step-Up in Basis? | Ability to Take Loans for Liquidity? |

| Taxable Account (No GRAT) | x | x | ||

| GRAT | x | x | ||

| Life insurance | x | x | x | x |

However, there are a couple of notable downsides when utilizing life insurance. The first is that traditional life insurance expenses can be quite high and eat up as much as 25%-30% of the gross return. The second is that it is difficult to dump-in a large amount of money at one-time into a life insurance policy the same way that you can with a GRAT.

However, the large expenses associated with life insurance can be removed by using private placement life insurance (PPLI). PPLI helps remove a majority of the expenses associated with traditional life insurance in exchange for the client contributing at least $1M-$2M in premiums into the policy. In exchange for the client doing this, the expenses in a PPLI policy are often reduced to 10%-15% of the gross return. So instead of the client paying 37%-50% of the gain in taxes, they are paying 10%-15% in insurance expenses.

Table 5: Comparing Taxes and Expenses of Different Vehicles

PPLI is the most cost effective estate planning tool. Instead of losing large amounts of the gross return to income and estate taxes, the client pays only 10% of the gross return in the form of insurance expenses.

| Estate Planning Vehicle | Gross Return | % Loss Due to Income and Estate Taxes | % Loss Due to Insurance Expenses | Net Return |

| Taxable Account | 8% | 71% | 0% | 2.30% |

| GRAT | 8% | 43% | 0% | 4.57% |

| PPLI | 8% | 0% | 10% | 7.20% |

As the above table shows, investing in tax-inefficient assets within a taxable account exposes the assets to both income and estate taxes. This is why in Example 1 we saw that John and Mary only earned a 2.30% net after-tax return even though the gross return was 8%. This meant that 71% of the return was lost to income and estate taxes.

A GRAT helps reduce the tax-drag through tax-deferred compounding, but as the above table shows 43% of the gross return is still lost to taxation. In contrast, the PPLI policy doesn’t lose any of the return due to taxes but has an insurance expense cost of 10%. Ultimately the net return of the PPLI after paying insurance expenses is significantly higher than that of just the taxable account or the GRAT alone.

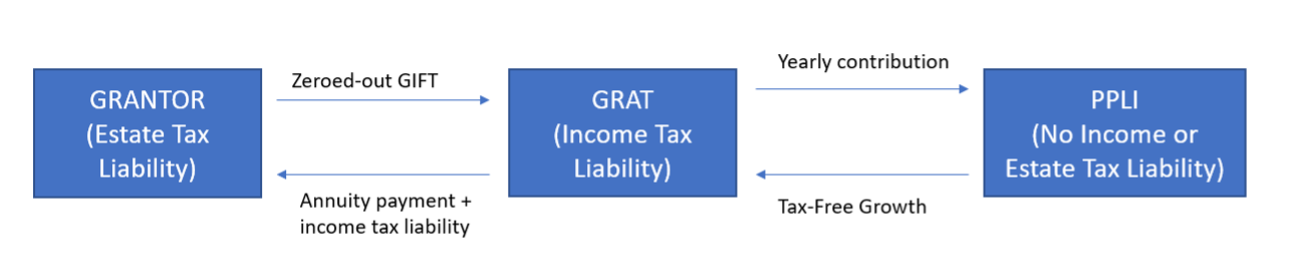

MOVING ASSETS FROM A TAX-DEFERRED GRAT INTO A TAX-FREE PPLI POLICY

While a PPLI policy can provide more cost-effective returns than a GRAT, the problem is that due to insurance limitations it’s much tougher to dump a large amount of assets into a PPLI policy all at once whereas it’s easier to do so with a GRAT. Therefore, it’s best to get assets out of the estate all at once using a Zeroed-Out GRAT and then contribute assets slowly over time to a PPLI policy from the GRAT. Essentially what the client is doing in this case is converting the tax-deferred returns of a GRAT into tax-free returns of the PPLI policy.

It’s important to remember that the grantor is paying taxes on the gains each year. If the GRAT reinvests the after-tax proceeds into tax-inefficient assets, then the gains are still exposed to taxes. However, if the GRAT takes those after-tax proceeds and invests them within a PPLI policy then future growth is tax-free without any tax-liability.

This essentially is the goal of using a PPLI policy with a GRAT; have the grantor pay the taxes to reduce the estate tax liability and then invest the after-tax proceeds into a PPLI policy to increase the wealth that accumulates outside of the estate by reducing the income tax liability.

Reducing the Income Tax Liabilities of a GRAT by Using PPLI

When a grantor moves assets into a GRAT, they are protecting assets from the estate tax but also creating a tax-income liability due to the loss of step-up in basis. By slowly moving assets from the GRAT to a PPLI policy, clients can reduce this income tax liability by moving the assets into a tax-free vehicle that is exempt from income and estate taxes.

In the below example, we take the same Example 1 assumptions from above but assume that the GRAT invests $3M each year into the same tax-inefficient assets, but instead using a PPLI policy instead of doing so via a GRAT.

Table 6: Utilizing PPLI to Improve Tax-Efficiency of GRATs

By utilizing a GRAT to facilitate investments into a tax-free PPLI policy, the clients are able to significantly reduce the tax-drag impact of the GRAT. The results in the after-tax IRR increasing by 32% (4.57% to 6.03%) by using a PPLI policy with the GRAT as opposed to just using the GRAT alone.

| Inside of Estate Assets at Death | Outside of Estate Assets at Death | Total After-Tax Wealth at Death | ||||||

| Market Value of Assets Before Estate Tax ($M) (A) |

Estate Tax Owed ($M) (B) |

Inside of Estate After-Tax Wealth at Death ($M) (C=A+B) |

Outside of Estate Assets Before Income Tax ($M) (D) |

Income Tax Owed ($M) (E) |

Outside of Estate After-Tax Wealth at Death ($M) (F=D+E) |

Total After-Tax Wealth at Death (G=C+F) |

Total After-Tax IRR (H) |

|

| No GRAT | $148 | ($49) | $99 | $0 | $0 | $0 | $99 | 2.30% |

| GRAT without PPLI | ($135) | $0 | ($135) | $337 | ($11) | $326 | $191 | 4.57% |

| GRAT with PPLI | $7 | ($3) | $4 | $286 | $0 | $286 | $290 | 6.03% |

The above table shows the impact of using a GRAT on inside of the estate wealth (Columns A through C), outside of the estate wealth (Columns D through F), and cumulative after-tax wealth (Columns G and H) which summarizes the total after-tax impact of using the GRAT vs not using the GRAT.

As the table above shows, using a PPLI policy with a GRAT helps to improve the after-tax IRR by 32% (4.57% to 6.03% as shown in Column H) as opposed to just using the GRAT alone. The reason for this is that it helps reduce the overall taxable gain of the GRAT since the assets are growing tax-free within the PPLI policy. This means that there is less tax that needs to be paid by the grantor and more overall after-tax wealth left to the beneficiaries.

USING DISCOUNTED VALUATIONS AND IN-KIND CONTRIBUTIONS WITH A PPLI POLICY

We can think of the use of a PPLI policy within a GRAT similar to that of a Roth conversion. The client contributes assets to a PPLI policy, pays any taxes owed on the gains at that point in time, and then any future appreciation grows tax-free. In order to see the value of this, it’s helpful to look at another example.

Example 3:

A trust is currently invested in a closed-end 10 year venture fund that invests in early stage startups does not allow for early liquidity. They have invested $5M into the fund (cost basis) and the market value of the fund is $10M. The trustee of the trust wishes to contribute the $10M position into a PPLI policy in-kind. Doing an in-kind transfer allows the trust to transfer the position to the policy without having to first sell an illiquid position at a reduced valuation (due to the illiquidity), contribute cash to the policy and reacquire the position within the policy. In order to transfer the position, the trust must first get an independent valuation of the position. Since the position is an illiquid position in a closed-end fund that invests in illiquid positions, the position would not be valued at the full $10M valuation of the underlying companies in the fund. The independent valuation agent determines that the fair market value of this position is $8M (a 20% discounted to the booked value). The trust would contribute the position in-kind to the PPLI policy. As a result of this transfer, the trust must pay income tax on the difference between the cost basis ($5M) and the discounted valuation ($8M). However, all future appreciation will be within the PPLI policy and tax-free.

In the above example, any future increases in the valuation would be tax-free. So for example, if at the end of the 10 year closed-end fund the position closes out at $50M, then all the appreciation above $8M would be tax-free. However, if this position remained in the trust then the trust would taxes on the full $45M gain between the $50M value and the $5M cost-basis.

PPLI AS A TAX-EFFICIENT ESTATE PLANNING TOOL

While PPLI policies have strict requirements with regards to investor control and diversification that are outside the scope of this article, and why it’s invaluable to work with a reputable estate attorney and advisors before engaging in the transaction, there are numerous advantages that PPLI policies can afford to estate attorneys and their clients as they look to move assets out of their estate in the most tax-efficient way possible.

DISCLAIMER: This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

About the Author

Rajiv Rebello, FSA, CERA is the Principal and Chief Actuary of Colva Actuarial Services and Colva Capital. Colva helps estate attorneys, family offices, and RIAs create better after-tax and risk-adjusted portfolio solutions for their UHNW clients through the use of life insurance vehicles and low-correlation alternative assets. He can be reached at rajiv.rebello@colvaservices.com. To learn more about PPLI, visit our website here.